[ad_1]

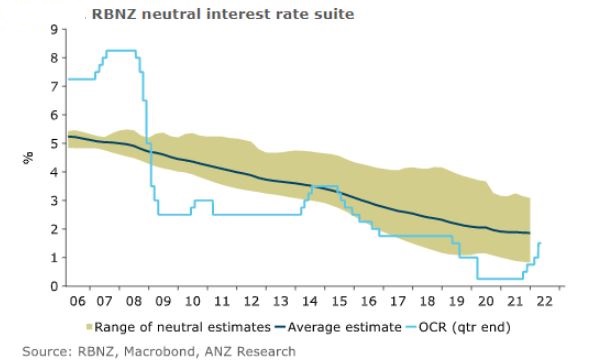

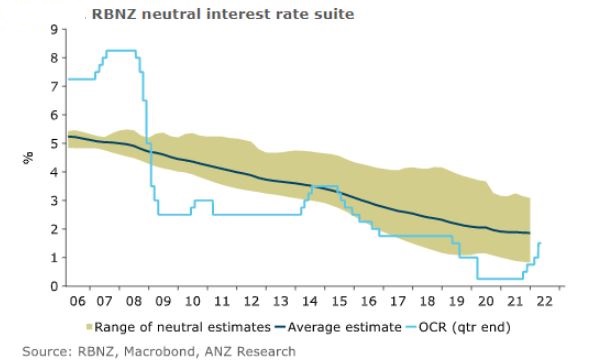

The Reserve Bank (RBNZ) is widely expected to increase the Official Cash Rate (OCR) by 50 basis points at Wednesday’s review, taking it to 2% which is the level the central bank currently views as neutral.

The neutral OCR rate is the level where it’s deemed to be neither stimulating nor constraining economic activity.

As ANZ’s economists led by Chief Economist Sharon Zollner put it, estimating the neutral interest rate is a difficult task at the best of times. And with COVID-19 disruption “still everywhere in the economic data,” it’s very difficult to accurately pin it down.

“However, we wouldn’t be too surprised if estimates of the neutral interest rate start to edge upwards, given the sharp rise in inflation expectations here and overseas. And it really matters what the RBNZ thinks neutral is, because they need to lift the OCR one for one with any increase in their estimate of neutral, otherwise interest rates can become more stimulatory, even if the OCR remains unchanged,” ANZ’s economists say.

Any upward revision in Wednesday’s Monetary Policy Statement would increase the odds the RBNZ isn’t finished with 50 basis points hikes after next week, ANZ suggests. The RBNZ increased the OCR by 50 basis points to 1.50% at its last review on April 13.

As ANZ’s economists put it, the policy outlook becomes more nuanced once interest rates are back into contractionary territory, or above the deemed neutral rate.

“Core inflation is clearly far too strong, and wages are accelerating. But at the same time, the RBNZ is hiking into a sharply slowing housing market. Our central forecast, which assumes no unforecastable downside risks materialise, predicts that the strong labour market will stop economic momentum from being completely flattened by the housing downturn.”

“But falling house prices have the potential to dent consumer spending, through wealth and/or confidence effects, and it’s a pretty unpleasant mix for the construction sector, with construction costs up 18% year-on-year in the first quarter, even as the end product (housing) is losing value,” ANZ says.

“In short, we think that the balance of risks around inflation and economic growth are likely to become less one-sided in favour of large OCR hikes over the second half of this year, and that should prompt the RBNZ to move in more considered 25 basis points steps over the second half of the year. But from this starting point, the tolerance for upward inflation surprises is nil.”

Zollner expects an OCR peak of 3.5% in the current cycle early next year.

‘Inflation is simply bonkers’

ASB Senior Economist Mike Jones also expect a 50 basis points increase. This, he says, is close to fully priced in by financial markets. However, what’s less certain is what the RBNZ does with its interest rate forecasts and forward guidance, which is what will shape Wednesday’s market reaction.

“Clouding the picture a little are rising recession risks, both globally and in NZ. These up the difficulty rating on the RBNZ’s future interest rate decisions but, for now, the focus will remain squarely on the problem at hand: inflation. Expect no quarter. The path of ‘least regret’ for the Bank is still to get the OCR to a neutral setting, about 2.0%, quick smart, then adopt a more cautious stance from there.”

“This front-loading approach will be enshrined in the Bank’s new OCR forecast track which we expect to show a much steeper ascent than the February Monetary Policy Statement, but not necessarily a much higher peak [of] 3.35% forecast in February. Something around 3.5% perhaps,” Jones says.

“There will also be interest in whether the backend of the RBNZ’s OCR forecast bakes in an assumption of an eventual easing cycle. The May Statement will show forecasts out to June 2025 so we think the track will tease eventual cuts. They’ll be modest though. The Bank won’t want the market to get fixated on this aspect and lose some of the tightening baked into the interest rate curve. We still don’t buy into the full extent of this implied tightening given the traction the Bank is already getting over demand, and in particular house prices.”

ASB’s economists forecast an OCR peak of 3.25% versus market expectations of about 3.75%.

Jones say although it can be argued that much of the inflation the RBNZ is fighting is outside its control because it’s either sourced offshore or reflective of supply shortages, NZ is in the midst of a negative supply shock coming on top of a positive demand shock. Annual inflation is running at 6.9%, the highest it has been since 1990.

“Inflation is simply bonkers and aggressive action is warranted to ensure it does not become embedded in expectations, which would necessitate a longer and more painful tightening cycle. The Bank’s own ‘stitch in time’ analogy remains apt.”

If a 50 basis points increase is delivered next week, the OCR will be at a neutral level, meaning the first part of the RBNZ’s job will be complete.

“From there, the least regret’s framework becomes more nuanced, necessitating a more cautious approach as the OCR enters territory on the tighter side of neutral. The Bank will likely move to a more data dependent approach as it seeks to balance restraining inflation expectations against risks of a hard landing down the line. We thus continue to expect the pace of hikes from July to November to slow to the regulation 25 basis points-per-meeting run-rate. Another 50 basis points lift in July remains a reasonable risk though and can’t be ruled out,” says Jones.

Bang for buck

Kiwibank Chief Economist Jarrod Kerr also expects a 50 basis points increase to 2%. He then expects 25 basis points hikes until the OCR hits 3% in November.

“And that should be enough. With house prices likely to be off 10% by year end, and most of the mortgage book refixing between now and then, the RBNZ is getting big bang for buck,” Kerr says.

According to RBNZ data, $206.5 billion, or 61.5%, of all residential mortgage debt will be affected by any rate increases over the next 12 months. That includes mortgages up for refixing and floating mortgages. As of March 31, there was a total of $335.447 billion worth of home loans outstanding.

Four consecutive 50 basis points hikes

Westpac NZ Acting Chief Economist Michael Gordon this week updated his forecasts, which now include four consecutive 50 basis points OCR hikes. Following the April increase and Wednesday’s expected one, Gordon sees additional 50 basis points increases in July and August, taking the OCR to 3%.

“That came out of two considerations. First, monetary policy settings are still a long way from where they need to be. We now expect the OCR to reach a peak of 3.50% for this cycle, from our previous forecast of 3.00%,” Gordon says.

“The second consideration was that the RBNZ’s change of tactics in the April review opened the door for larger OCR moves in the future. The April decision was described as ‘a stitch in time saves nine’ – early action to get on top of inflation would reduce the risk of having to lift interest rates to an even higher level in the longer term.”

“We agree with the reasoning behind this. There is understandably a concern about the impact that higher interest rates will have on highly indebted property owners, especially those who got into the market recently when interest rates were at their lows. But the RBNZ would do them no favours by going easy on them at first, then ultimately having to lift interest rates well above what was considered to be the pain threshold,” Gordon says.

Westpac notes house prices have now fallen for five consecutive months.

An unemployment headache

As reported earlier in the week, BNZ Head of Research Stephen Toplis believes the RBNZ has little option but to hike the OCR by 50 basis points on Wednesday. Toplis argues the lowest unemployment rate in decades, 3.2%, is a bigger headache for RBNZ monetary policy than the highest inflation in 30 years.

“The Reserve Bank’s task is clear. At its most basic level it has to get current annual inflation of around 7% down to 2% and it will require the unemployment rate, now 3.2%, to rise to around 4.5% to meet its maximum sustainable employment objective.”

“The only way the RBNZ can achieve this is to keep raising interest rates until it gets the traction it desires. And so it will,” says Toplis.

[ad_2]

Source link

{kind=link}