[ad_1]

A law meant to correct the harm done by decades of discrimination in bank loans is undergoing a long-awaited overhaul.

Fair lending advocates have said it’s too easy for banks to get a passing grade under the Community Reinvestment Act, and that communities of color continue to be disproportionately denied home loans. Now federal regulators are working on a significant update to CRA regulations.

Enacted in 1977, the law requires banks to meet the credit needs of communities where they operate. Today, though, many customers rely on mobile and internet banking services that are inconsistently covered by the CRA. And bank branch closures have accelerated throughout the nation, disproportionately impacting low-to-moderate income areas and communities of color.

Under the new rule, proposed earlier this month, bank performance evaluations by the Federal Deposit Insurance Corp., the Federal Reserve Board, or the Office of the Comptroller of the Currency would be tailored to a financial institution’s size and business model. Availability and responsiveness of mobile and online banking would be one of the items regulators look at for large banks. Regulators clarified activities that would count toward a bank’s performance grade, such as teaming up with community development financial institutions and lending to affordable housing projects.

The public has until Aug. 5 to submit comments about the proposal.

Fair lending advocates have long called for modernizing the CRA, which they say has not kept pace with changes in the banking industry. The Opportunity Finance Network, a national network of more than 370 community development financial institutions, has partnered with banks looking to reach underserved communities but said lack of clarity in CRA rules was a stumbling block.

“It hasn’t always been clear whether or not those activities that banks are undertaking with us will actually count for them to get CRA credit on their exams, especially if they’re happening outside of their assessment areas,” said Dafina Williams, the network’s senior vice president of external affairs. As a result, she said, some banks have been reluctant to lend or invest with community development financial institutions.

Under the current rules, banks are assessed based on their performance in geographical areas where they have physical locations. The proposed changes would also give banks credit for working with community development financial institutions in other places.

“There’s a lot of need in communities outside of those assessment areas, and especially when you think about rural markets and Native communities where there’s really not a lot of physical locations for banks to be evaluated,” Williams said.

She believes the proposal could do more to improve racial equity. While current performance evaluations consider mortgage lending data only on the basis of income, the proposal calls for large banks’ evaluations to also consider how mortgage lending has been distributed by race and ethnicity. Williams would also like to see that information for small business lending.

While the disclosure of mortgage race and ethnicity data alone won’t impact a bank’s ratings under the proposal, the data along with additional signs of discrimination might.

Buzz Roberts, CEO and president of the National Association of Affordable Housing Lenders, said the CRA regulations are in great need of an update.

“Communities of color — especially predominantly Black neighborhoods — have not been receiving home mortgages at a rate that would even maintain their low rates of homeownership, let alone enough to close homeownership gaps with white neighborhoods,” he said in an email.

A history of discrimination in bank lending

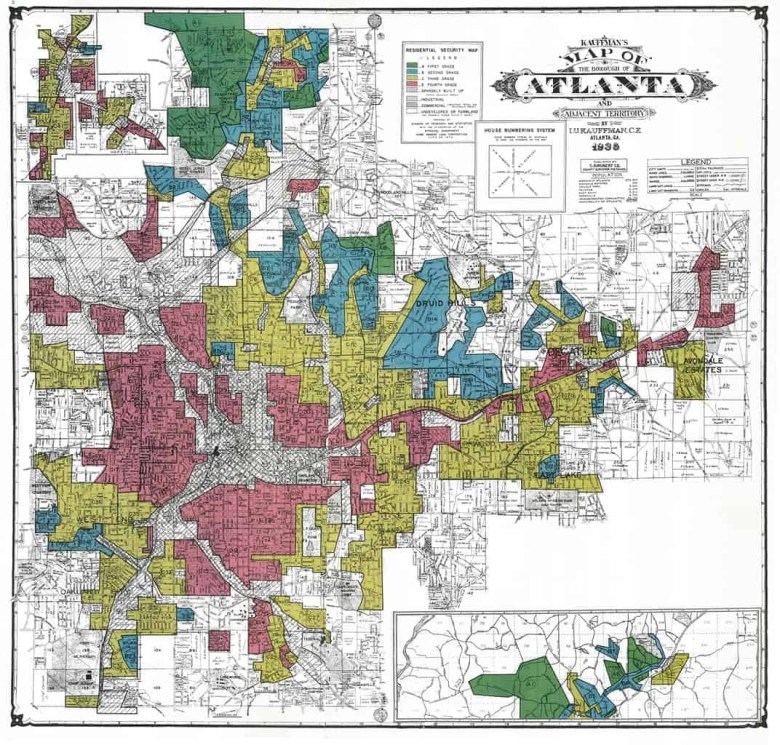

Redlining — a discriminatory practice in which neighborhoods where people of color lived were deemed too hazardous for investment, and banks denied loans there — was not only legal in the U.S. for decades but also federal policy.

In the 1930s, redlining maps created by the Home Owners Loan Corp. color-coded neighborhoods based on race, class, ethnicity, housing conditions or proximity to pollution sources. The Federal Housing Administration and the Veterans Administration followed similar practices. Generations of disinvestment followed.

“Those neighborhoods, over a period of 80 years, labored under enormous economic disadvantage,” said Josh Silver, a senior policy advisor at the National Community Reinvestment Coalition. “The white middle class was created from homeownership, and African Americans were locked out of that.”

Congress took several steps to end the decades of discrimination, starting with the Fair Housing Act in 1968. The Equal Credit Opportunity Act in 1974 prohibited discrimination in lending, while the 1975 Home Mortgage Disclosure Act requires lenders to collect ethnicity data for home loan applicants and borrowers. The CRA, passed two years later, requires banks to serve their communities, including low- and moderate-income neighborhoods.

About every three or four years, banks undergo a performance review by federal regulators. The results are publicly available, and public comments are included in evaluations. FDIC regulates state-chartered banks that are not Federal Reserve Board members, the Federal Reserve Board regulates state-chartered member banks, and the Office of the Comptroller of the Currency regulates national banks and federal savings associations. Institutions’ lending patterns count for half their grade, with investment and services making up the rest.

Banks receive one of four ratings in a pass or fail framework. When a bank fails, it is more difficult to acquire new branches or merge with other banks, and they are subject to more frequent CRA exams.

CRA has been effective, to a degree. Banks made more than $883 billion in loans for affordable housing and economic development projects as well as 24 million small business loans in low- and moderate-income communities between 1996 and 2015, for instance.

But the National Community Reinvestment Coalition believes that the CRA examinations do not accurately reflect banks’ performance. Only about 2% fail, according to the coalition.

In consideration of race

Redlining has had generational impacts on wealth-building in communities of color. Historically redlined areas now have greater levels of poverty and higher prevalence of poor mental health than communities that were not deemed hazardous on historical maps, according to a National Community Reinvestment Coalition study.

But the CRA focuses on income, not on how banks serve people of different races.

An Office of the Comptroller of the Currency spokesperson said the agency “would not speculate” on why the law was designed that way. But Silver, with the National Community Reinvestment Coalition, has an idea.

“The law does not talk about race, and that is likely because the senator who was the main sponsor, William Proxmire, calculated that it probably would not have passed Congress if it mentioned race,” he said.

At the time, a backlash to affirmative action was evident in Regents of the University of California v. Bakke, a 1978 Supreme Court decision that held that a racial quota system for school admission violated the Constitution’s Equal Protection Clause.

Roberts, with the National Association of Affordable Housing Lenders, wishes the proposed CRA changes would be more explicit about what it means for a bank to serve, as the law puts it, “the credit needs of its entire community.”

“It is disappointing that the proposal would not directly consider home mortgage and small business lending to people and communities of color,” he wrote in an email.

Silver would like to see CRA exams look at lending to underserved census tracts and areas that historically experienced redlining. If banks are graded on it, they’ll hopefully do more of it, he said.

“This will hopefully start redressing the injustice that had been perpetuated for 80 years against those communities,” Silver said.

[ad_2]

Source link

{kind=link}