[ad_1]

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

HO-5 insurance offers comprehensive coverage for homeowners. Learn more about what it covers, how much it costs, and how it differs from other policies. (Shutterstock)

Homeowners insurance comes in many different forms that vary based on the type of home you have and the level of coverage you want. You have eight different options for homeowners insurance coverage, which range from HO-1 to HO-8. Of these, HO-5 is the most comprehensive.

Here’s a look at what HO-5 insurance is, what it covers, and how much you can expect to pay for this type of homeowners insurance policy.

Credible makes it easy to compare homeowners insurance quotes from top carriers.

What is HO-5 insurance?

An HO-5 policy covers your home’s structure, any detached structures (such as a garage), and your personal property. It provides open-perils or all-risk protection, meaning it covers damage from any peril (like fire), unless your policy expressly excludes it. This differs from HO-3 insurance, the most common type of homeowners insurance, which offers open-perils coverage for your home but not your belongings.

3 MAJOR HOME INSURANCE MISTAKES TO AVOID

Why do you need HO-5 insurance coverage?

If you have a mortgage loan, your lender will typically require you to purchase homeowners insurance. This will protect you and your lender if your home burns down, sustains hail damage, or gets taken out by a tornado — your policy will help cover the costs to repair or rebuild your home.

Even if you don’t have a mortgage, homeowners insurance is essential, since most of us can’t afford the out-of-pocket costs to completely replace our homes. After all, if a fire destroys your home, you’ll need to replace it and everything that was inside. This means buying everything from new clothes to furniture and electronics. Without insurance coverage, you’re on the hook for every single one of those replacement purchases.

With HO-5 insurance coverage, you get comprehensive protection for your home and your personal belongings against virtually all risks. This means that your insurance coverage will help you out under many circumstances, unless the peril is specifically excluded in your policy. HO-5 insurance is especially helpful for new or more expensive homes, since it offers expanded coverage for valuables.

What does HO-5 insurance cover?

While other types of coverage (such as HO-1 and HO-2) only cover named perils (events specifically listed in your insurance policy), HO-5 insurance covers all possible perils, unless they’re explicitly excluded. An HO-5 policy offers coverage in six different areas:

- Your home’s structure (Coverage A)

- Other structures on your property (Coverage B)

- Your personal property (Coverage C)

- Additional living expenses if a peril makes your home uninhabitable (Coverage D)

- Personal liability if someone injures themselves on your property or you cause damage to someone else’s property (Coverage E)

- Medical payments if you accidentally cause injury to someone else (Coverage F)

While each policy and carrier may differ in terms of exclusions, HO-5 insurance generally protects against damages from perils like:

- Fire

- Smoke

- Lightning

- Hail

- Wind

- Tornadoes

- Weight of ice, snow, or sleet

- Damage from aircraft

- Explosions

- Theft

With Credible, you can compare homeowners insurance quotes from multiple carriers in minutes.

What does HO-5 insurance exclude?

When it comes to HO-5 insurance, your policy covers all perils except any that are specifically excluded. For that reason, it’s important to ask your carrier about exclusions before purchasing coverage, and to read your policy documents very carefully.

However, homeowners insurance policies have some common exclusions, such as floods, earthquakes, sewer backups, and acts of war. In addition, your homeowners insurance won’t cover damages related to neglect or normal wear and tear.

WHAT IS A HOME INSURANCE DEDUCTIBLE?

How much HO-5 insurance should you get?

An HO-5 policy covers both your home and the property inside it, so you’ll want to purchase enough coverage to protect both categories. It’s a good idea to purchase enough coverage to completely replace your home in the event that it’s destroyed. The same is true for your belongings. To determine the amount of coverage you need, you’ll need to do the following:

- Calculate the replacement cost of your home. You can estimate this number by multiplying the total square footage of your home by local per-square-foot building costs. For a more accurate number, you can hire an appraiser to inspect your home.

- Calculate the total value of the personal property in your home. You can typically choose between actual cash value and replacement cost when covering your belongings. Actual cash value will pay you for your belongings according to their current value, taking depreciation into consideration. Replacement cost will reimburse you for a similar item at today’s prices, no matter how old it is. To calculate the replacement cost of your personal property, create an inventory of everything you own. Note the item and the price to replace it with something comparable today. Once you’ve completed your inventory, add up the numbers to get your total.

Buying too much coverage can mean wasting money on annual premiums. Buying too little coverage, however, could leave you holding the bag if your home and personal property are destroyed. Take your time when determining how much homeowners insurance to buy.

How much does an average HO-5 policy cost?

The cost of homeowners insurance coverage can vary greatly depending on your location, the age and style of your home, and the level of coverage you choose, among other factors.

In the U.S., the average cost of an HO-5 policy was $1,412 per year in 2019, or just under $118 a month, according to the National Association of Insurance Commissioners.

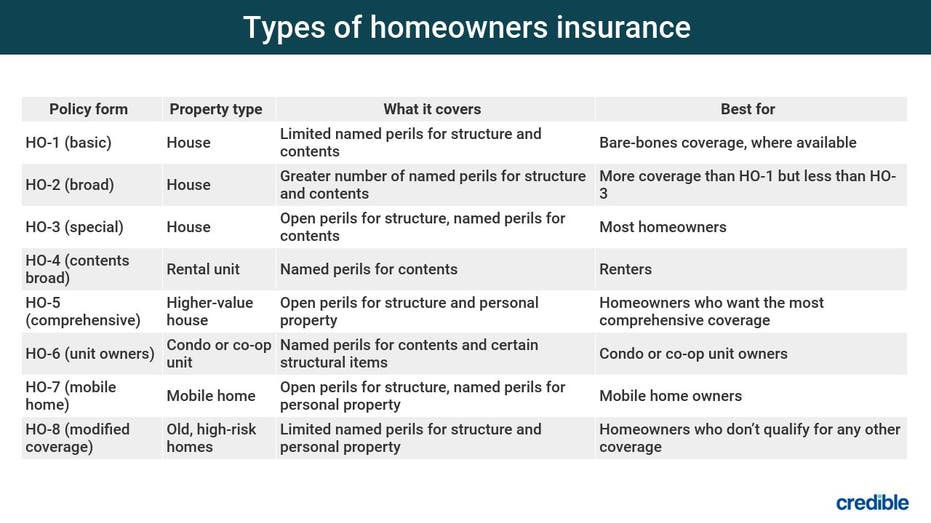

How is an HO-5 policy different from other policies?

Homeowners insurance coverage comes in eight different forms, each offering its own level of coverage. Here’s how they differ and what makes HO-5 coverage unique.

How to purchase home insurance

If you’re looking to buy a homeowners insurance policy, either for an existing property or for a new home, you’ll need to follow these steps:

- Calculate how much coverage you need, and determine which type of policy works best. Once you know how much coverage you need, you can decide on the policy type that suits you best. When you determine your needs for dwelling and personal property coverage, you can set your policy limits accordingly.

- Shop around and compare quotes. Spend some time getting quotes from multiple carriers to see who has the best rates and coverage for your situation. Many insurance providers will let you get a quote online, though you may also need to speak with an agent.

- Set your deductible and select optional coverages. Once you have a carrier and policy picked out, it’s time to personalize the coverage. This means selecting a deductible if you didn’t while getting quotes. Your deductible is the amount you’ll be responsible for paying out of pocket following a covered event. You can also purchase any optional coverages you want (like flood or earthquake protection).

- Purchase the policy and pay your premium. After personalizing the policy that works best for you, the final step is to buy it. You can choose to pay your annual premium up front or spread it out in installments. Keep in mind, your mortgage lender may require you to pay premiums through an escrow account, building them into your monthly mortgage payment.

Check out Credible to compare homeowners insurance quotes from various providers, all in one place.

[ad_2]

Source link

{kind=link}