[ad_1]

As mortgage rates rise, consumers are pivoting away from cash-out refinances and toward HELOCs, a shift that many lenders are looking to take advantage of going forward.

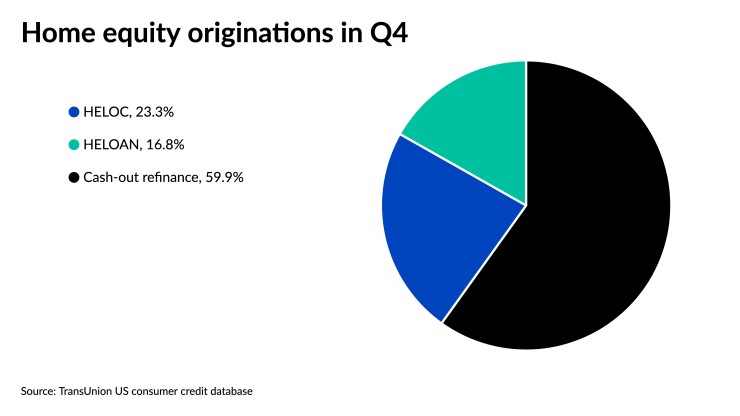

TransUnion reported the volume of new home-equity lines of credit increased in the fourth quarter of 2021 by 31% year over year, from 212,303 to 278,230. Home-equity loan originations also grew by 13%. But in the same annual period, cash-out refinances declined by 6%, despite rates hovering near 3% for a good part of last year.

As a combined total, home equity originations increased to 1.2 million in volume over the final three months of 2021, up 4% from the fourth quarter of 2020 and 80% above year-end 2019.

The data suggests that “for those who are already homeowners, the continued home-price appreciation offers an opportunity to tap into growing home equity and gain access to cheaper capital,” said Joe Mellman, senior vice president and mortgage business leader at TransUnion, in a press release.

The amount of tappable home equity accelerated further in the fourth quarter, reaching an all-time high or approximately $20 trillion, up from $18 trillion three months earlier, according to TransUnion.

“We saw HELOC and HELOAN improve in the most recent quarter, and that may continue here in the coming months.” said Dan Simmons, senior director financial services consulting at TransUnion, in a webinar detailing the research findings.

With the report including only data collected at the end of 2021, the findings did not factor in activity that resulted after the steep spike in interest rates in the first four months this year. Although mortgage rates trended upward toward the end of 2021, recent, sharper increases have further reduced incentive for borrowers to refinance, making HELOCs a more appealing option.

“Mortgage lenders can bolster growth in a subdued market by leveraging tools that can identify and reach consumers who are in the market to tap their available home equity,” said Mellman.

Some are already heeding that advice. The higher-rate environment has led to large reductions in both originations and profits at several nonbank mortgage companies, as reported in first-quarter earnings. As a result, some are actively trying to develop new offerings to drive business. In May, both loanDepot and New Residential announced the introduction of HELOCs to their portfolio of products. In loanDepot’s earnings call, Executive Chair Anthony Hsieh cited client demand for them despite few marketing efforts from his company.

“Customers are very savvy and starting to ask for HELOC by name, certainly because they don’t want to touch the 2% to 2.5% historical-low 30-year interest rate that they obtained over the last one to two years,” Hsieh said.

The rise in tappable home equity since 2018 also coincides with the emergence of fintechs specifically serving clients trying to tap into home equity. Since last summer, the likes of Hometap, EquiFi and Button Finance have all benefited from venture-capital funding. Other fintechs in the market include Noah and Unison.

In its Q1 2022 Credit Industry Insights Report, TransUnion also reported mortgage-origination growth declined by 27.5% on an annual basis in the fourth quarter to 2.93 million loans, consisting of 55.6% in purchases, 24.4% cash-out refinances and 20% rate-and-term refinances. In the third quarter, volumes experienced a 12.6% drop, while in the fourth quarter of 2020, loan originations increased by over 73%. Originations data comes from the prior quarter to account for reporting lag.

New mortgage balances decreased 23% to $860 billion from $1.1 trillion in the fourth quarter of 2021, the first fall in annual growth since 2018. But the median balance of new loans increased 2% year over year to a record $258,000. Mortgages backed by Fannie Mae and Freddie Mac accounted for 51% of the balance, while new jumbo loans made up 18%. Federally guaranteed mortgages took an approximate 17% share.

Across all consumers, TransUnion noted the improvement in credit-risk profiles since 2018, particularly since the pandemic’s onset. In the first quarter, 76% of consumers landed in risk categories of prime or above compared to 71% before the emergence of coronavirus. A number of borrowers previously with subprime profiles improved their credit scores through the help of government and lender assistance introduced during the pandemic. Credit scores have risen to 708 from 685 in the first quarter of 2018, based on VantageScore 4.0 system calculations.

“Excess liquidity and lender programs allowed consumers to pay down balances,” Simmons said. “They also reduced their utilization rates and avoided delinquencies, three of the major factors that comprise credit scores.”

[ad_2]

Source link

{kind=link}