[ad_1]

Life Insurance Corporation (LIC) stock made a tepid listing at the bourses in May. Since then, the stock of India’s biggest life insurer has been unable to come up to the IPO price of Rs 949. Emkay Global Financial Services, a leading domestic brokerage has initiated coverage on the stock with a ‘hold’ rating with a target price of Rs 875 – up around 8 per cent from the current levels.

The brokerage, however, feels LIC is an ‘elephant that can’t dance’ and lists key reasons for its belief. “While we appreciate LIC’s market-leading position and comfortable valuations, we prefer private sector peers that have better growth, profitability and therefore higher return on Embedded Value (RoEV) prospects,” wrote Avinash Singh and Mahek Shah of Emkay Global in the report.

ALSO READ | LIC Q4 result review: Hits, misses, and the road ahead for investors

Here are the key reasons for their rating.

LIC’s valuation attractiveness more optical than fundamental

LIC’s IPO valuation of Rs6 trillion, or the current market cap of Rs 5.3 trillion, according to Emkay, appears undemanding considering its H1FY22 Embedded Value (EV) of Rs 5.4 trillion and the listed private peer valuation multiple of around 2.0-3.6x on FY22 enterprise value (EV). The composition of LIC’s EV, its growth prospects and its volatility, Emkay said, create lots of uncertainties.

LIC’s value of new business (VNB) accretion at around 1-1.5 per cent of EV from FY25 fares poorly with around 8-11 per cent of EV being accrued as value of new business (VoNB) for private sector peers, Emkay said. In addition, LIC’s EV is largely an outcome of par and non-par fund bifurcation exercise undertaken in H1FY22.

ALSO READ | LIC booked Rs 42,000 cr profit from equity markets in FY22

“Without this bifurcation exercise, LIC’s H1FY22 EV would have been Rs 1.25 trillion, instead of Rs 5.4trillion. Further, a very significant portion of this EV is sitting in the form of mark-to-market (MTM) gains in equity investments backing the non-par liabilities, taking EV sensitivity to equity market fluctuations to a substantially higher level,” Emkay said.

Operational challenges beneath the mammoth size

With a legacy of 65 years and around 45 years of that being a monopoly, LIC’s mammoth size, Emkay believes, seems to be hiding a number of current and future challenges. For one, Emkay suggests that LIC’s commission and cost structure are bloated. That apart, it has an exceptionally higher share of single-premium business, especially in group fund-based businesses and has negligible unit-linked and retail protection businesses.

“Adjusted for these peculiarities, a number of operational challenges are reflected in the recent year data. LIC has lost market share materially in retail annualised premium equivalent (APE) in the last 5 and 10 years. The market share loss has accelerated in the last 5 years. Despite the mammoth scale, the cost ratios are very high,” Singh and Shah wrote.

Changing product and distribution mix is a difficult task

Though LIC intends to change its product mix materially in the coming years to arrest a fall in its market share and improve new business margins, analysts at Emkay remain skeptical of a material and sharp change in the product mix.

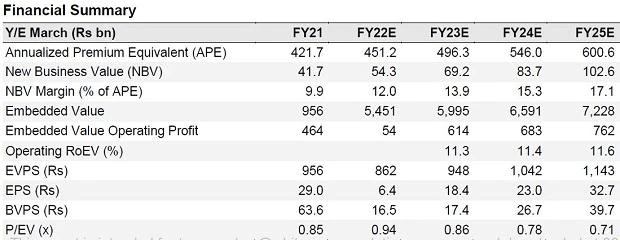

Table Source: Emkay Global report

Dear Reader,

Dear Reader,

Business Standard has always strived hard to provide up-to-date information and commentary on developments that are of interest to you and have wider political and economic implications for the country and the world. Your encouragement and constant feedback on how to improve our offering have only made our resolve and commitment to these ideals stronger. Even during these difficult times arising out of Covid-19, we continue to remain committed to keeping you informed and updated with credible news, authoritative views and incisive commentary on topical issues of relevance.

We, however, have a request.

As we battle the economic impact of the pandemic, we need your support even more, so that we can continue to offer you more quality content. Our subscription model has seen an encouraging response from many of you, who have subscribed to our online content. More subscription to our online content can only help us achieve the goals of offering you even better and more relevant content. We believe in free, fair and credible journalism. Your support through more subscriptions can help us practise the journalism to which we are committed.

Support quality journalism and subscribe to Business Standard.

Digital Editor

[ad_2]

Source link

{kind=link}