[ad_1]

Westpac expects the cash rate to rise to 1.75 per cent by the end of this calendar year, from 0.35 per cent today, and to 2.25 per cent in 2023. The bank also forecasts house prices in Sydney and Melbourne to fall by 9 per cent next year.

Guided by its chief economist, Bill Evans, Westpac expects the economy to expand by 4.5 per cent this year, but then to slow to 2.5 per cent in 2023 as rate rises start to bite. This was similar to the RBA, which said on Friday GDP would grow by 4.25 per cent this year and fall to 2 per cent in 2023.

The impact of a 25 basis point rise in the economy is bigger than it used to be.

— Peter King, Westpac CEO

Westpac forecasts credit growth rising by 5.7 per cent this year but slowing to 4.3 per cent in 2023, as higher interest rates reduce borrowing capacity. However, it said on Monday it was willing to lend more to property investors to support the market.

The bank said it expected many recent borrowers to cut discretionary spending next year given they had less time to build up buffers. Three years ago, it fought the corporate regulator in the so-called “wagyu and shiraz” case, in which the Federal Court found Westpac had not broken responsible lending laws. The bank made its own assessments of borrowers’ loan-servicing capacity instead of following the regulator’s guidelines because borrowers could reduce their spending on luxury items.

Mr King said the big banks had originated about a quarter of all their mortgages in the past two years, and it was this cohort who might have to curtail spending on things such as home renovations, fancy holidays, restaurant meals and entertainment as rates rise.

“More of people’s income will be spent on housing, whether that is rental or mortgages, and depending on what type of rate cycle we see, there could be less income available for other discretionary spending,” he said.

“It’s a pretty tricky balancing equation for the Reserve Bank as it goes through the next period, and we have got higher leverage – so the impact of a 25 basis point rise in the economy is bigger than it used to be.”

Curbed enthusiasm

On a $500,000 loan, an additional 2 per cent in rates equates to $10,000 a year in after tax income paid to banks.

“That is what people have to be thinking about – they have got to be getting prepared for it, and it is probably going to be the way money is spent that will change in the broader economy,” Mr King said.

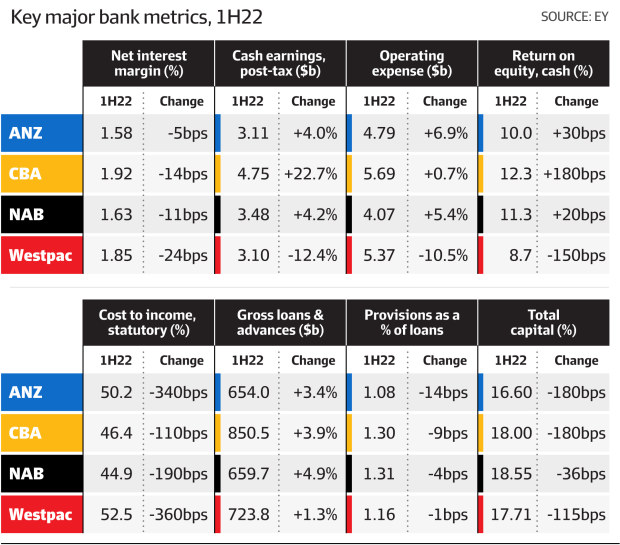

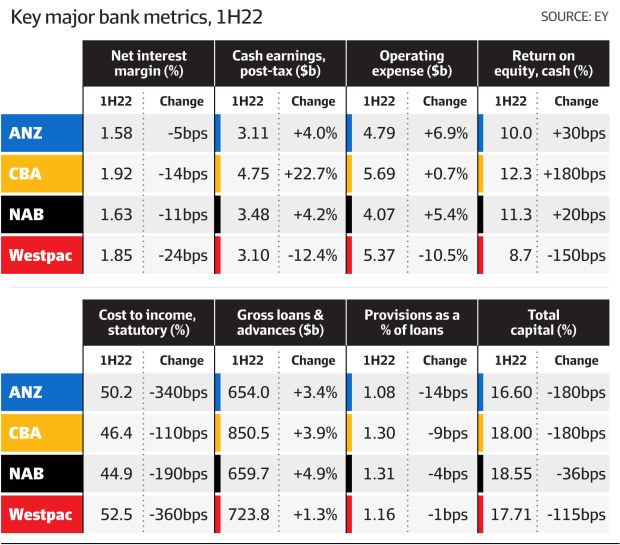

Mounting uncertainty about the effect of rising rates curbed enthusiasm on the interim results of the big four banks, which reported combined cash earnings of $14.4 billion, up 5.1 per cent on the first half of 2021 after growth in business and housing lending as the economy rebounded from the pandemic. Bank profits lifted as bad debts fell even further, supported by record low levels of unemployment.

However, cost pressures and intense mortgage competition squeezed net interest margins as management took the knife to expenses to maintain profits, the latest interim reporting season revealed.

Westpac remained committed to its target of reducing overall costs to $8 billion by 2024 despite rising wage pressures, with 4000 staff cut during the half. ANZ and National Australia Bank walked away from previous cost targets, saying rising inflation had changed the game.

Across the sector, total operating expenses at the big banks decreased by only 1 per cent to $4.9 billion, KPMG found, as inflation drove up “run-the-bank” costs. Banks also continued to invest more in technology to guarantee they could compete in the digital economy by transforming legacy IT systems.

Staying the course

Justifying maintaining its cost target, Mr King said Westpac needed to move more aggressively than rivals because its overall cost base was larger. He said it had made gains selling non-core businesses, reducing office space (including offshore locations) and cutting the number of transactions done in branches as it moved more products to digital platforms.

Advisers and investors said banks faced many uncertainties that would keep them under pressure in 2023 and 2024, despite the resilient performance so far this year.

“The only thing that is certain is uncertainty,” said Tim Dring, who leads EY’s banking and capital markets practice in Oceania.

“Supply chains, geopolitical issues, wage pressures, and as interest rates move up to combat inflation, there’s also uncertainty around how households will cope with those higher rates.”

Bank stocks have performed well this year as the market factors in more revenue from higher interest rates, given bank net interest margins should increase as they widen the spread between the rates charged to borrowers and those paid to savers. Strong capital levels should also support more capital being returned to shareholders.

But some fund managers think the risks of rising rates could outweigh the positives. Romano Sala Tenna, a portfolio manager at Katana Asset Management, was reducing exposure to banks. He reckons bad debts must have finally hit a low point now that rates were rising, which would also reduce borrowing capacity.

“With rates going up, we are going to see lower growth in lending, and we are going to see mortgage book stress at some time. You are also going to see wages and other cost escalation,” Mr Sala Tenna said.

[ad_2]

Source link

{kind=link}